Last month we detailed both the tax and control issues that come with a Trump Account. This month we’re discussing four existing alternative options that have more favorable tax treatment. With each of these options you’ll also be able to invest in a wide variety of choices compared to a Trump Account, which essentially only allows investment in an S&P 500 or similar index fund and nothing else until a child turns 18.

Roth

A Roth is usually the best option if a child is eligible for one. To be eligible they must have earnings from some sort of work, which most newborns don’t have. All growth is 100% tax-free and gains can be taken out at zero tax for all the same reasons that would waive the 10% tax penalty for taking money out of a Trump Account, such as education, first-time homebuyer, reaching age 59 ½, etc. Unlike with a Trump Account, whatever was originally contributed to a Roth can be taken out at any time and for any reason with no tax at all. Since any contributions from family would be after tax with both a Trump Account and a Roth and the Roth has all gains tax-free, the Roth is a superior option for any child eligible to have one. Just like with a Trump Account, there is a limit on how much can be contributed each year and the child will gain full control of the money at age 18, which are a couple of bigger downsides.

529

Unlike with a Roth or Trump Account, a 529 allows a parent, grandparent or other family member to maintain complete control of the money indefinitely and can actually change who the money is for at anytime. Not only can the account be changed to another family member, but also to oneself. Additionally, unlike a Roth or Trump Account, there is a Kansas tax deduction for contributing to a 529. One can receive a tax deduction of up to $3,000 (which could save $174 in state tax) per year for each person they are making a 529 contribution for. So, if a married couple had two kids, that would mean up to $12,000 (each person contributing $3,000 to each child) could be contributed per year, which would save nearly $700 in state taxes for most. While more can be contributed each year to a 529 than this, there would be no tax break on the additional amounts. If the money is used for education, then all of the growth becomes tax-free. In recent years, the definition of what counts as an education expense has expanded greatly to include a lot of options besides traditional college, such as private K-12 tuition and expenses, student loan repayment, and apprenticeship programs. If a child never ends up needing the money for education expenses, which was always a concern in the past, up to $35,000 can now be converted to a tax-free Roth.

UTMA

UTMA stands for Uniform Transfers to Minors Act and is an account that a parent or other person would control and be in charge of until the child turns either 18 or 21. At that point the child would have full control of the account, just like with a Roth or Trump Account. Unlike a Roth or Trump Account, though, there is no limit on how much can be contributed to a UTMA and in most cases up to $2,700 a year in interest, capital gains, and/or dividends can be made in the account completely tax-free. A UTMA account invested in an S&P 500 index fund, as is required in a Trump Account, would need to be over $150,000 in value before there would be any federal tax on the dividends. Even above this amount, the tax would be less on a UTMA account than a Trump Account on any gains and with a UTMA account the money can be used for any purpose and at any time without a tax penalty. Once a child comes of age, they could potentially sell investments and realize up to $66,500 worth of gains each year at zero federal income tax too.

Brokerage Account

This last option really offers the most flexibility as the owner maintains complete control at all times, can invest in anything, can have money withdrawn for any reason, and can have an unlimited amount deposited into it. Who the money is for can also be changed to anyone at any time too. The drawback to this option is that the owner, whether it be a parent, grandparent, etc. would be responsible for paying yearly any taxes owed on any interest or dividends paid. For most, though, this would be a very minimal amount if tax-efficient ETFs are utilized. At any time, the owner can gift shares to a child’s UTMA or, if they are over 18, that person’s investment account. Doing that would then shift the tax of selling any investment to the child’s tax return, which in many cases would be a lower tax or potentially no tax at all. This is a common tax saving strategy we utilize with our clients.

What Should You Do Now

Generally, we suggest starting with a Roth if a child is eligible, then a 529. We caution against putting too much into a 529, though, unless you’re confident that the money will be used for education expenses in the future. Ideally, you would want the 529 to not grow in value to more than $35,000 when the child turns 18 as that is how much could be switched to a Roth tax-free if the money isn’t used for education. After that, most people then look at utilizing a brokerage account, though we do have a few clients that use UTMAs.

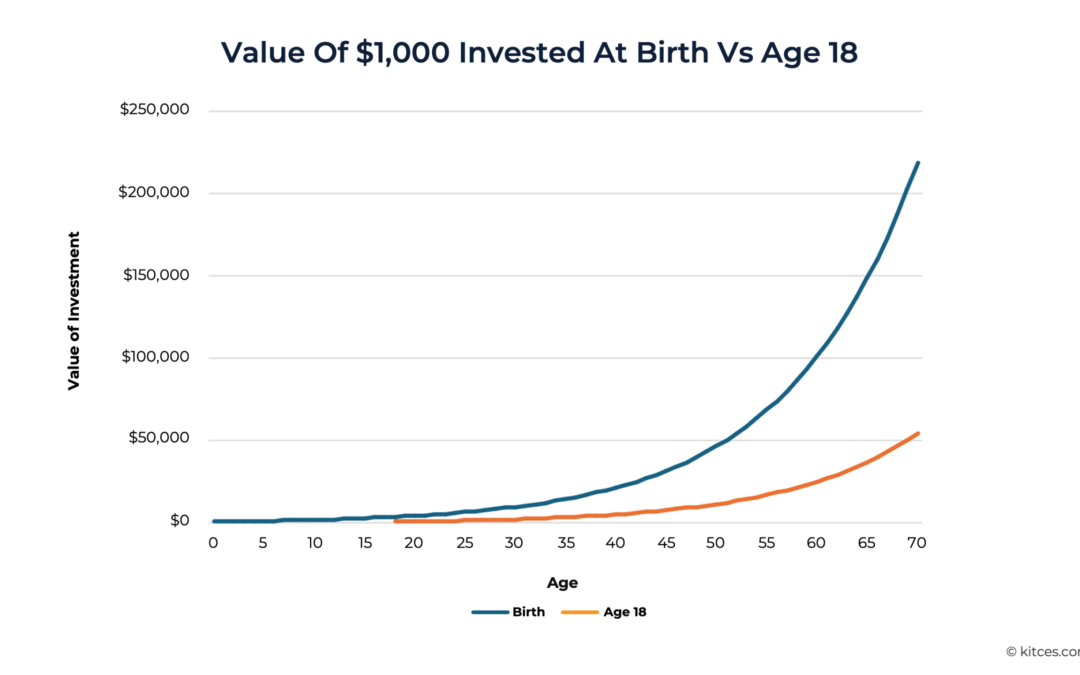

Regardless of the direction you select, the most important thing is to save as early and often as possible. Don’t be paralyzed by all the choices and let analysis paralysis lead you to doing nothing. As shown in the chart, starting with $1,000 at birth versus at age 18 leads to a very significant difference later in life even with a conservative 8% return projection. If you’d like help determining what might be the best route for your situation, you can set up a complimentary strategy session with a financial advisor on our team at Retirement Portfolios in Lawrence by calling 785-330-9292 or filling out the form below.

Recent Comments